(Note: this post first appeared on the Investing with Trends blog.)

Summary

The BOXX ETF provides returns that closely track those of Treasury bills. Due to a quirk in the US tax code, BOXX ETF profits are taxed as capital gains, not investment income. That means that long-term holders of BOXX pay long-term capital gains rates which can be much lower than ordinary income tax rates. Investors who hold Treasury bills in taxable accounts should consider replacing them with BOXX.

The risk-free rate and Treasury bills

The risk-free rate is an important concept in the capital markets. It is defined as the theoretical rate of interest that investors receive on investments that have zero risk. The risk-free rate does not really exist in practice, as all investments have non-zero risk, even if it is small.

Investing in Treasury bills comes close, though. Treasury bills are short-term debt instruments (with maturity of less than 12 months) issued by the US federal government. The US does not have a perfect credit but it is still excellent. US debt is rated AA+ by Standard & Poor’s and Fitch, and Aaa by Moody’s. Treasury bills are highly liquid instruments that currently offer yields over 5%. Many investors increased their allocations to T-bills as yields rose from zero and stock market valuations reached stratospheric levels.

The main downside of T-bills is their tax treatment. Interest received on T-bills is treated as investment income for federal tax purposes, subject to tax rates of up to 37%. However, the interest is exempt from state and local taxes.

The risk-free rate and box spreads

We mentioned that the risk-free rate is a theoretical construct as there is no such thing as a completely risk-free investment. But apart from Treasury debt, there are other investments that closely track the risk-free rate with minimal risk. One of those are box spread strategies in the options market.

Box spreads behave similarly to short-term debt and they have been widely used by option market makers for decades. When a market maker has excess cash, he can buy box spreads to receive income. When a market maker needs to borrow money, he can sell box spreads and pay interest rate close to the risk-free rate. Box spreads (or boxes) feature cheaper interest rate than that offered by a clearing house and are thus quite popular. They are also highly liquid, offering an easy way to borrow or lend on short notice without any lockups.

How do boxes work?

Box spreads may look like a complex strategy but their underlying logic is simple. A box consists of four legs: two calls and two puts, with two different strikes. Let’s look at an example.

We will trade European options (to simplify some wrinkles around dividends), such as options on the S&P index future. We will use two strike prices: 5000 and 5100, and add the following positions:

- long call at 5000

- short call at 5100

- short put at 5000

- long put at 5100

What happens at expiry?

If the price P at expiry is less than 5000, the calls expire worthless. The long put position will be worth 5100 - P, the short put position will be worth P - 5000. The total value of the box will be 5100 - P + P - 5000 = 100.

If the price P at expiry is greater than 5100, the puts expire worthless. The long call position will be worth P - 5000, the short call position will be worth 5100 - P. The total value of the box will be P - 5000 + 5100 - P = 100.

And what if the price P ends up between 5000 and 5100? Both short positions (the 5100 call and the 5000 put) will expire worthless. The long call position will be worth P - 5000, the long put position will be worth 5100 - P. The total value of the box will be P - 5000 + 5100 - P = 100.

No matter where the price ends, we will receive 100 which is the difference between the two strikes.

How much is this position worth? Because there is no price risk, the buyer should receive the risk-free rate of interest (or close to it) from the seller. If we are 90 days away from expiry and the interest rate is 5%, the box should trade at 98.79 (assuming quarterly compounding).

We now have a simple strategy for generating income. Every quarter, we buy a box spread where the strikes are 100 apart. This will cost 98.79 and pay 100 at maturity. Repeat this four times a year and receive interest income similar to that of buying Treasury bills.

Counterparty risk

The nice thing about boxes is that the counterparty is the clearing house, not the trader on the other side of the trade. Index options are trading on the CME which has AA- rating and clears its own trades. Equity options are cleared by the Options Clearing Corporation (OCC) which has AA+ credit rating. Both the CME and the OCC are Systemically Important Financial Market Utilities under the Dodd-Frank Act of 2012. They are subject to enhanced prudential standards and tighter regulation than other financial institutions. Even though there is no explicit government guarantee of their liabilities, it can be assumed that the US government would step in if they ran into trouble.

Tax treatment of box spreads in an ETF

So far, we have managed to replicate a Treasury bill with a lot of extra effort. What is the point of all this? The real attraction of box spreads is their tax treatment once they are wrapped inside an ETF.

On their own, box spreads suffer from complex tax rules. If the options’ underlying consists of futures or broad market indexes, they are treated as Section 1256 contracts. That means that 60% of their gain or loss is taxed at long-term capital gains rates and 40% at short-term capital gains rates, regardless of the actual holding period. Section 1256 contracts are also taxed on their unrealized gains and losses at calendar year end.

If the underlying consists of stocks or ETFs, the tax rules get even more complex. Depending on whether the position was closed, expired, or exercised, it can be taxed at short-term capital gains rates, long-term capital gains rates, or it can be rolled into the cost basis of the underlying instrument.

What is common to all these rules, however, is that the income received from box spreads is taxed as capital gains, not as investment income. That makes a huge difference when the positions are held inside an ETF.

ETF tax rules mandate that investment income received by the ETF has to be paid out to investors as dividends. Dividends arising from interest income are treated as unqualified and subject to ordinary income tax rates. Investors in ETFs holding T-bills pay federal taxes on their dividends, but not local and state taxes.

However, income received from selling box spreads is not interest income, it is capital gains. Technically, ETFs do not buy and sell the securities they own, they receive and redeem them in kind from authorized participants. This is not the place to go deep into ETF creation and redemption mechanics but the upshot is that ETFs, unlike mutual funds, do not distribute to investors capital gains on their holdings. Investors in ETFs only pay capital gains taxes when they sell their positions. If they hold the ETF longer than one year, they will benefit from lower long-term capital gains rates.

By putting box spreads inside an ETF, we have achieved financial alchemy. We have generated interest income that is taxed at capital gains rates. This is an amazing loophole in tax rules that nobody had foreseen when those rules were written.

BOXX ETF

The first box spread ETF, with the ticker BOXX, was launched by Alpha Architect on Dec. 28th, 2022. Even though Alpha Architect has downplayed the tax benefits of BOXX, trying to avoid too much attention from the IRS, the BOXX ETF has gathered $1 billion in assets in the first year of its existence. The word is starting to get out and inflows are strong. For comparison, the biggest Treasury bill ETF (BIL) has gathered $31 billion in AUM in the 17 years since it launched.

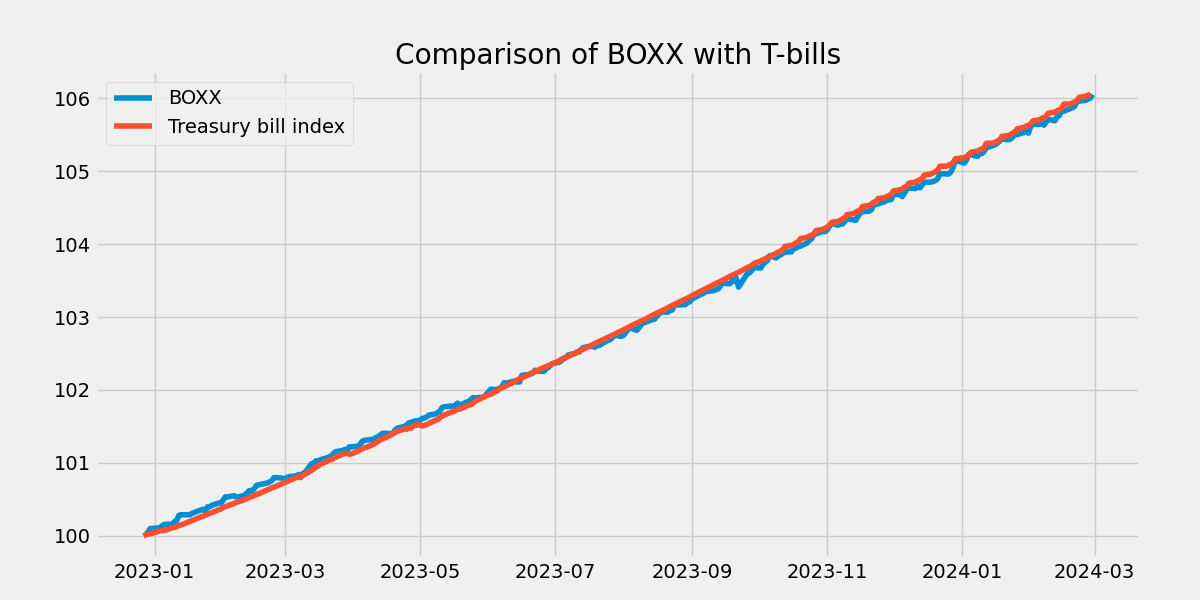

BOXX has tracked Treasury bills quite well, lagging behind by less than its expense ratio (0.195% per year).

Conclusion

Investors who hold Treasury bills or T-bill ETFs in their taxable accounts should take a look at BOXX and take advantage of its tax benefits. If investors held BOXX for less than one year, they would pay the same federal tax rates as T-bill holders (but BOXX holders would not benefit from state and local tax exemptions). If they held BOXX for more than one year, however, the tax rate would drop significantly. For an investor in the highest tax bracket, the rate would go from 37% to 20%. Capital gains taxes would be deferred and only get paid when the BOXX holding was sold, unlike income taxes on T-bill interest which are due each year. Furthermore, capital gains on BOXX can be offset by losses on other holdings, which is not the case for interest income received from T-bills.

As always, please consult with your tax advisor to see whether these benefits apply to your situation.